Table of Content

Depending on the circumstances, Freddie Mac requires a score of 620 or 660 for a single-family primary residence. If you are a veteran or an active military member, you are eligible for a flexible, low-cost VA loan. These are known as non-conforming loans, meaning they are designed to be held by the lending institution for the duration of the contract and will not be transferred to another financial institution.

The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. Refinance disclosure - By refinancing the existing loan, the total finance charges may be higher over the life of the loan. Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy.

When Does A Conventional Loan Make More Sense For You?

It all comes down to what makes the most sense for you, which is why it’s so important to shop around and compare loan options before making a decision. If you’re eligible, a VA loan can often be the better choice between an FHA loan and a VA loan. This is because VA loans allow borrowers to get into a home with zero down and no mortgage insurance.

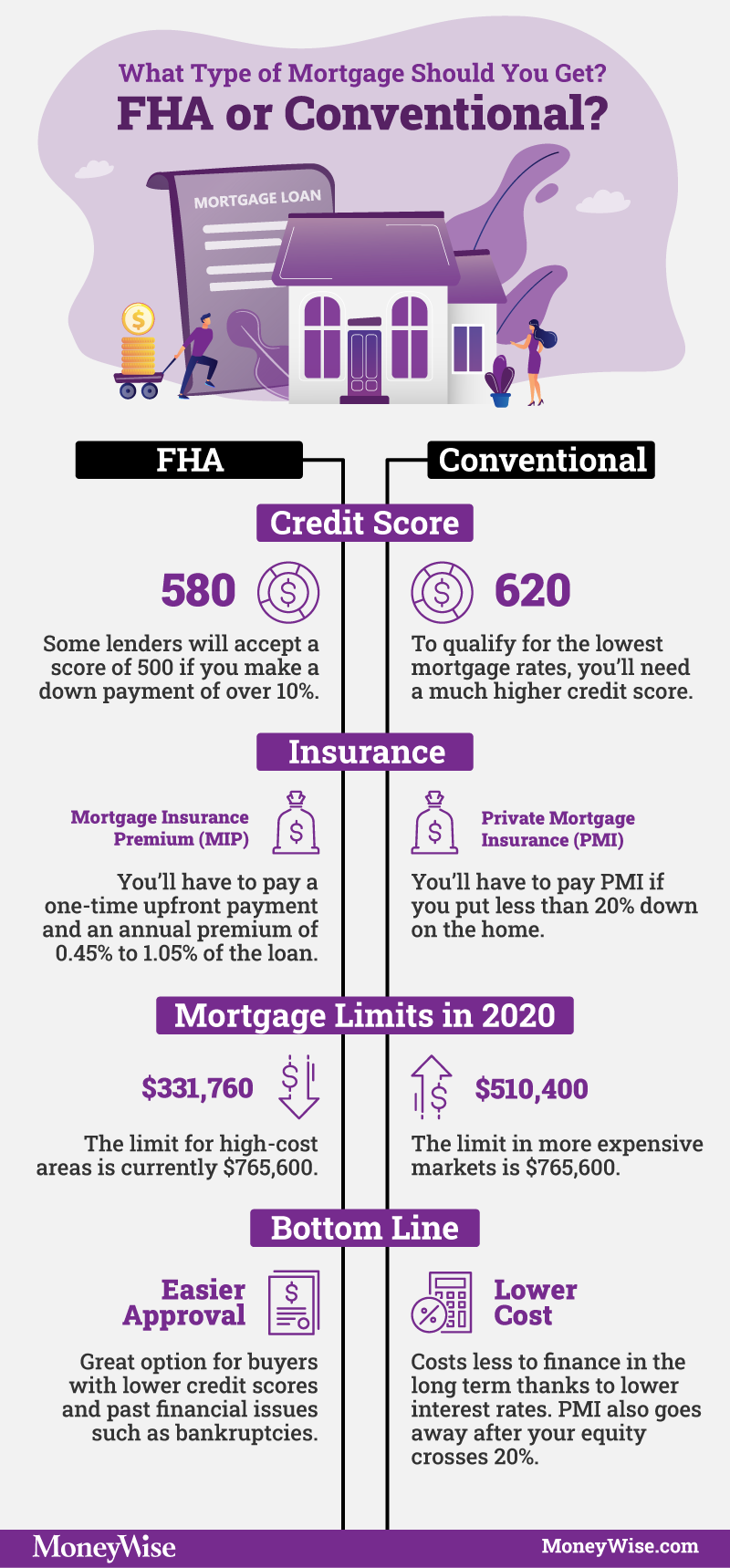

However, you only pay the insurance until your principal balance is less than 80% of the home’s value. FHA borrowers do pay mortgage insurance for the life of the loan. The FHA charges upfront mortgage insurance equal to 1.75% of the base loan amount.

Comparing Conventional, FHA and VA Loans

FHA loans are government-backed by the Federal Housing Administration and generally have more flexible qualification criteria than conventional loans. VA loans are also guaranteed by the federal government through the U.S. Department of Veterans Affairs and cater to active-duty military, veterans and surviving spouses. A VA loan is a mortgage option that is fully backed by the U.S. As a result of this guarantee, VA mortgages require no private mortgage insurance and make the qualification process easier. They typically have more favorable interest rates and conditions than other loan types, including conventional loans.

Because VA mortgages are non-conforming, they must be held by their lender or sold to another – but not Fannie Mae or Freddie Mac. Non-conforming loans also include jumbo loans, Federal Housing Administration loans and U.S. Regardless of your down payment on the VA loan, you’d still end up paying the VA funding fee, whereas you’d be able to avoid paying PMI with a down payment of 20% or higher on a conventional loan. The lack of PMI could result in a lower monthly payment on a conventional loan compared to financing with a VA loan. Housing market conditions, inflation and even the Federal Reserve all factor into current mortgage rates.

Loan Officer Email Form

A significant difference between VA and conventional loans is that VA loans are only for primary residences. The primary residency requirement doesn't rule out duplexes or fourplexes, but to use a VA loan, you must intend to live in the property you purchase. With FHA mortgages, this is referred to as an FHA Streamline Refinance.

VA loans have no down payment requirement, so homebuyers can finance up to 100 percent of the purchase price of their home. Homeowners can refinance up to 100 percent of their home's value, or in some cases even higher. The money goes directly to the Department of Veterans Affairs and is used for general program costs, as well as to cover losses.

Debt-to-income ratios are calculated by dividing all your monthly expenses by your gross monthly income. Lenders utilize this ratio to measure a borrower’s ability to make monthly home loan payments. In addition, insurance is usually required if the down payment is less than 20%. Share ThisIf you plan to buy a home, you are undoubtedly considering the various types of loans to finance your purchase. VA loans have a specific range of interest rates, benefits and qualification requirements.

However, borrowers usually have to pay a funding fee—a one-time charge between around 1.25% and 3.6% of the loan amount. What credit score do I need to get a conforming conventional mortgage loan? Depending on the situation, Fannie Mae generally requires borrowers to have a credit score of 620 or 640.

So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. At Bankrate we strive to help you make smarter financial decisions. While we adhere to stricteditorial integrity, this post may contain references to products from our partners.

Homebuyers who need a mortgage and homeowners who want to refinance an existing loan have many options from which to choose. Remember that conventional loans are usually better suited for borrowers with a higher credit score, while FHA and VA loans can be ideal for those with a lower score. FHA offers refinance options, such as a streamline refinance.

Conventional loans are backed by private lenders such as banks and credit unions. You and the property have to qualify, but this depends on standard factors, such as income level or credit score. The loan rates and APR calculations also assume certain facts according to the type of loan described. Conventional loans do not have any unique fees like the VA funding fee.

No comments:

Post a Comment